A customer asks for an invoice in a format your team can't generate. Finance says the invoice is already electronic because it's sent by email as a PDF. IT says they can export XML, but they're not sure whether the customer, portal, or government channel will accept it. Procurement wants this resolved quickly because payment depends on it.

That's the point where “digital invoicing” stops being a vague project and becomes an operational risk.

For Austrian companies and any business trading into the EU, the essential question isn't whether you can create an invoice on a computer. It's whether your invoice is in a structured, compliant, machine-readable e invoicing format that can pass validation, move through the right delivery channel, and land in the recipient's system without manual rework. That distinction affects public-sector tenders, cross-border interoperability, tax readiness, and day-to-day accounts receivable efficiency.

A lot of teams find out too late that a PDF solves the human reading problem, not the system processing problem. Buyers, government entities, and networks increasingly expect invoice data that ERP and AP platforms can validate automatically.

Table of Contents

- Introduction Why Your PDF Invoice Is Not an E-Invoice

- What Defines a True E-Invoice Format

- A Guide to Common E-Invoicing Formats

- Navigating Austrian and EU E-Invoicing Mandates

- How to Choose the Right E-Invoicing Format

- Implementation Best Practices for Finance and IT

- Common Questions on E-Invoicing Formats

Introduction Why Your PDF Invoice Is Not an E-Invoice

The confusion usually starts with language. People say “electronic invoice” when they mean any invoice sent digitally. In practice, that's too broad to be useful.

A PDF sent by email is digital, but that alone doesn't make it a true e-invoice. The problem is simple. A human can read a PDF easily, but a finance system can't rely on it as structured business data unless there's a compliant machine-readable payload behind it.

That difference matters the moment a customer asks for automated processing, a public buyer requires a specific standard, or your AP and AR teams want invoices to post without rekeying. A PDF may look complete on screen and still fail the receiving system's checks because the required data isn't encoded in the right syntax.

Practical rule: If the recipient's platform needs to validate fields automatically, a visual document alone won't be enough.

For finance directors, this isn't a technical side issue. It affects three core outcomes:

- Compliance exposure: A non-accepted invoice format can delay submission or rejection.

- Cash flow friction: If the buyer can't ingest the invoice, payment usually slows down.

- Internal cost: Staff end up correcting, converting, and resending invoices manually.

In Austrian and EU-facing operations, the decision about e invoicing format should be treated like any other control decision. You need to know what data the invoice must contain, what syntax the recipient accepts, how it must be transmitted, and how it will be archived. Once teams separate “document appearance” from “machine-readable structure,” format selection becomes much easier.

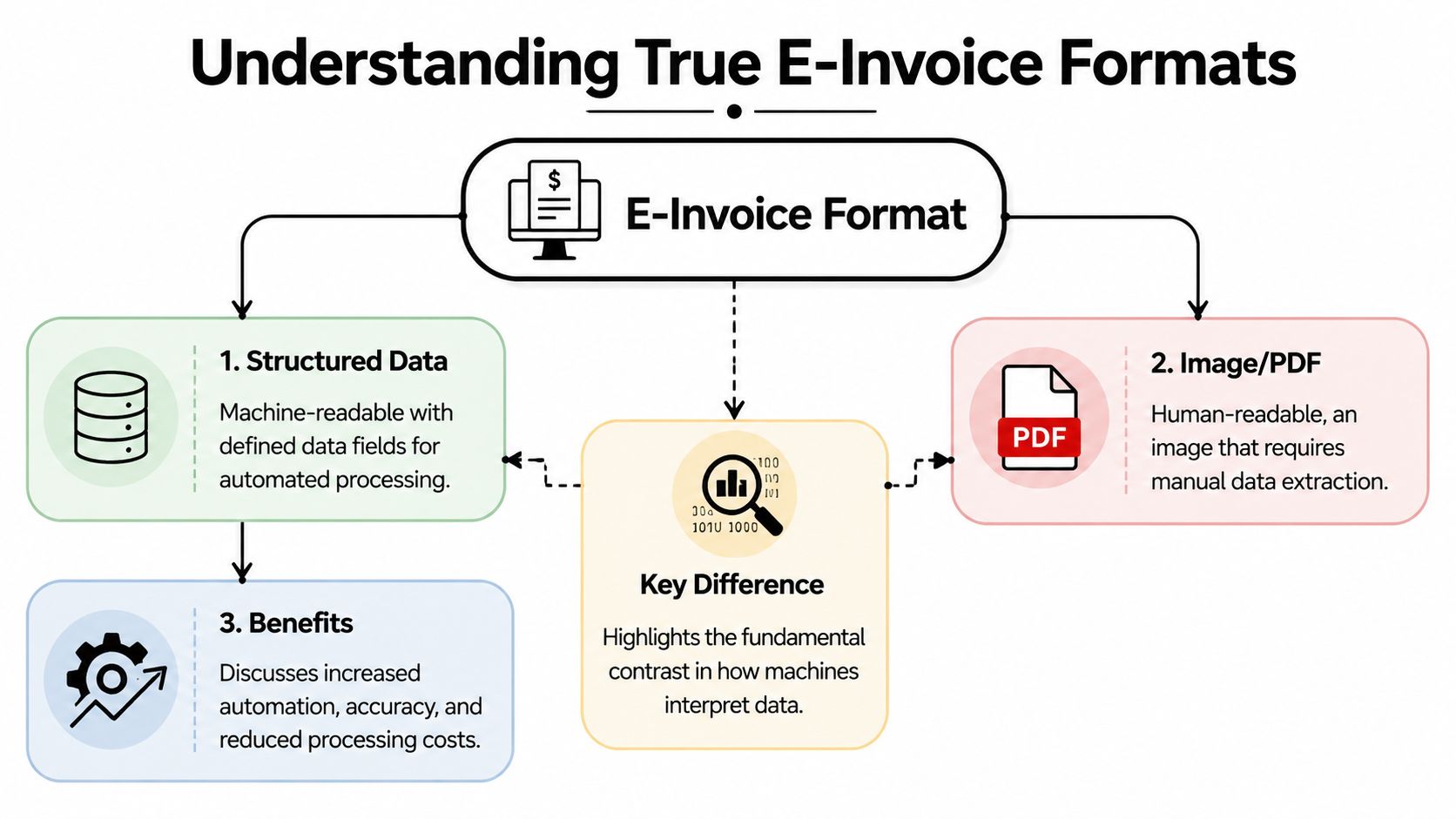

What Defines a True E-Invoice Format

A useful way to think about this is to compare a scanned spreadsheet with the actual spreadsheet file. The scan shows the same numbers to a person, but the software can't reliably work with rows, columns, and formulas. The file can.

That's the core distinction in e invoicing format selection. A real e-invoice is built for systems first, humans second.

Structured data is the real requirement

A frequently missed issue is whether a PDF invoice counts as an e-invoice. Tungsten Automation's explanation of machine-readable invoice formats makes the key point clearly: a PDF can be transmitted electronically, but it is not machine-readable by default, while structured formats such as XML, EDI, CSV, UBL, and JSON are designed for automated ingestion into ERP and AP systems.

In practical terms, a structured invoice doesn't just show “invoice date” or “tax amount” on the page. It tags those values so software knows exactly what each field means. That allows validation, routing, tax checks, matching, and posting logic to happen automatically.

Here's where businesses usually get caught out. They assume email delivery equals e-invoicing readiness. It doesn't. If your customer, portal, or network expects structured content, your PDF is only a picture of an invoice.

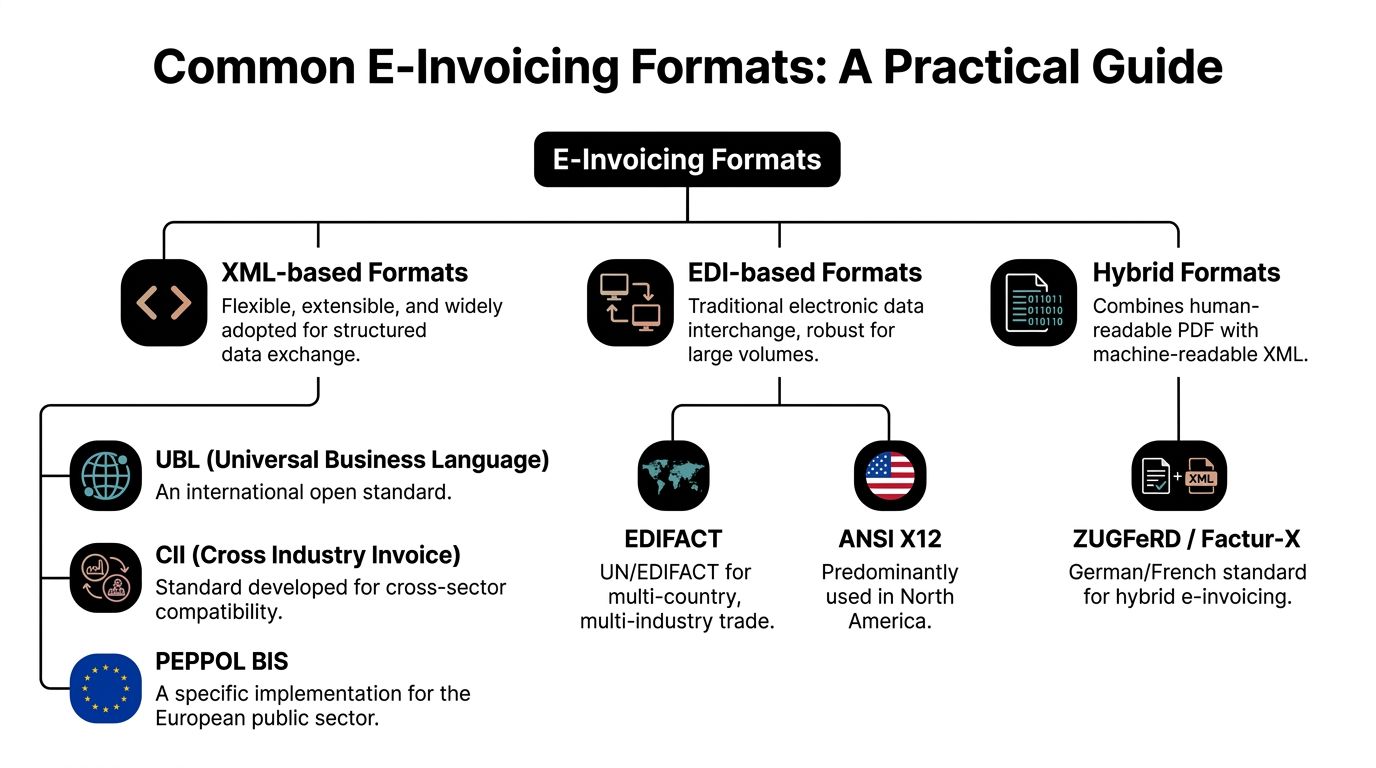

Three format families matter in practice

Most businesses deal with three broad categories:

| Format type | What it is | Operational reality |

|---|---|---|

| Unstructured | PDF, Word, image files | Good for human reading, weak for automation |

| Structured | XML, UBL, CII, EDIFACT, JSON | Built for system-to-system exchange |

| Hybrid | PDF with embedded XML | Useful when both people and systems need the same artifact |

Each has a place, but they solve different problems.

- Unstructured documents work when the recipient is willing to read and key in data.

- Structured formats work when the recipient wants validation and straight-through processing.

- Hybrid formats can help in mixed environments where some users still need a readable PDF while the system consumes the embedded data.

A document that looks right to a person can still be wrong for the receiving platform.

That's why the term e invoicing format should never be reduced to “file type.” The core issue is data structure, validation logic, and acceptance by the destination system.

A Guide to Common E-Invoicing Formats

Some formats are best understood as base syntaxes. Others are implementation profiles built on top of those syntaxes for a specific network, country, or use case. If you blur those layers together, projects get messy fast.

The core languages

The most common interoperable syntaxes are UBL and CII. Ecosio's guide to e-invoice syntax and transmission notes that XRechnung implementations in Germany must be transmittable in either UBL or CII, and that the Peppol network primarily uses UBL BIS Billing 3.0, a UBL subset optimized for cross-border exchange.

That tells you something important. UBL and CII are not random alternatives. They are core machine-readable languages that many real-world e-invoicing models build on.

Other formats also appear in live environments:

- EDIFACT still matters in established EDI trading relationships, especially where large-volume B2B integration already exists.

- JSON may appear in modern API-based ecosystems, but acceptance always depends on the target platform's rules.

- CSV can be machine-readable in a broad sense, but it usually isn't enough for regulated, standards-driven invoicing on its own unless a recipient specifically accepts it.

Network and country profiles

The next layer is where many finance teams get tripped up. They choose a syntax but ignore the destination profile.

A buyer may say “send UBL,” but that often means “send UBL that conforms to our network profile and business rules.” That's a narrower requirement.

For companies working across Austria and neighboring markets, you'll commonly run into:

- Peppol BIS for networked exchange and public-sector interoperability

- XRechnung when dealing with German public-sector requirements

- Country-specific profiles that add field rules, code lists, and validation expectations on top of a base syntax

If your team needs a grounding in network-based exchange, this overview of Peppol e-invoice basics for Austrian businesses is a useful reference point.

Later in the evaluation process, it helps to see the concepts explained visually:

Hybrid formats for mixed environments

Hybrid models are often the most misunderstood.

Formats such as ZUGFeRD and Factur-X combine a readable PDF with embedded XML. That can be practical when suppliers, auditors, and internal users still want a document they can open easily, while the receiving system needs machine-readable content.

Use them carefully. Hybrid doesn't mean “any PDF with some data inside.” The embedded structured layer must still conform to the required standard and business rules. If it doesn't, the invoice may appear fine to a person and still fail automated acceptance.

The safest way to think about formats is this:

Choose the syntax for interoperability, the profile for compliance, and the channel for successful delivery.

Navigating Austrian and EU E-Invoicing Mandates

Legal requirements changed the market long before many companies changed their habits. That's why format choices now sit much closer to compliance than to simple document preference.

Why the EU mandate changed format decisions

A major turning point was the public-sector mandate under European Directive 2014/55/EU. Seeburger's background on the EU e-invoicing milestone explains that the directive made e-invoicing progressively mandatory for public procurement and accelerated the move from paper and PDF invoices to structured formats across Europe.

That shift matters because it pushed buyers, vendors, ERP providers, and public platforms toward structured exchange, validation rules, and auditable processing. In Austria and across the EU, today's compliance-focused environment makes much more sense when you see that history.

For a finance leader, the practical takeaway is straightforward. Public-sector invoicing isn't just “send us a bill electronically.” It usually means sending data in an accepted structured format through an accepted route.

What Austrian suppliers need to check

If you supply Austrian public entities or trade with EU customers that follow public-sector style controls, don't stop at the file format. Check the full acceptance model:

- Recipient scope: Is the customer a federal authority, another public body, or a private-sector buyer with its own integration standard?

- Accepted syntax: Do they require UBL, CII, a profile derived from them, or a hybrid form?

- Transmission path: Must the invoice go through a portal, a network, or a direct B2B connection?

- Archiving obligations: Can you retain the legal invoice in a way that preserves authenticity and readability?

For a concise operational overview, the summary of Austrian e-invoicing requirements is worth reviewing before implementation starts.

Delivery failure is another area teams underestimate. If an invoice is technically correct but never reaches the right destination or gets rejected in the handoff, finance still has a problem. That's why this CISO guide for invoice delivery failures is useful reading for control design and exception handling.

Compliance doesn't end when the XML is generated. It ends when the invoice is accepted, traceable, and archived properly.

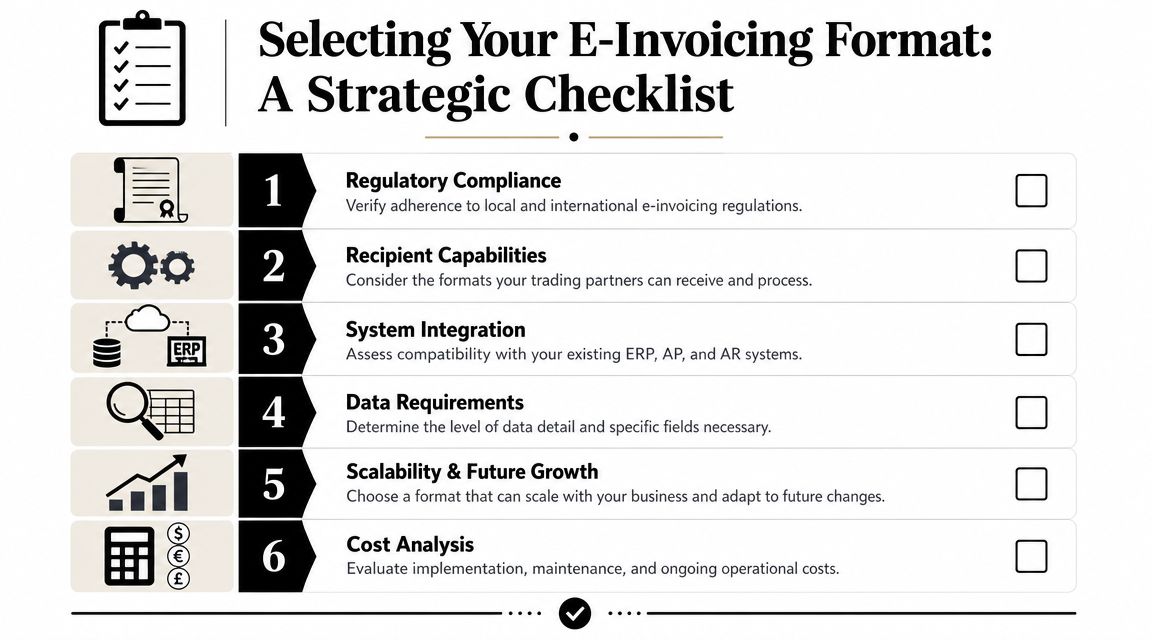

How to Choose the Right E-Invoicing Format

There isn't one universally best format. There is only the format that fits your counterparties, your systems, and your compliance perimeter.

That means the wrong way to choose is to ask IT what your ERP can currently export and stop there. The right way is to start from acceptance and work backward.

Start with the recipient not your current output

The most useful framing I've seen is this: the practical question isn't just which format is machine-readable, but which one will survive tax, archiving, and trading-partner requirements across jurisdictions. NRD Companies' discussion of e-invoicing requirements across jurisdictions captures that business reality well.

Start with a short decision map:

Who receives the invoice

A public buyer, a large enterprise, and a smaller private customer often have very different acceptance rules.How they receive it

Through Peppol, a government portal, private EDI, or direct system integration.What legal record counts

In some setups, the structured payload is the operative invoice even if a PDF view is also available.What your ERP can generate reliably

Native support is better than repeated conversion if volume and complexity are growing.

Match the format to your operating model

Different situations call for different choices.

| Business situation | Usually the better fit | Main trade-off |

|---|---|---|

| Public-sector or networked exchange | UBL-based profile | Strong interoperability, stricter validation |

| Established enterprise EDI relationships | EDIFACT or existing EDI model | Stable for current partners, less flexible for new mandate-driven use cases |

| Mixed human and machine use | Factur-X or ZUGFeRD | Easier readability, but XML quality still decides acceptance |

| Multi-country growth | Standards-based structured model | More setup discipline upfront, less fragmentation later |

A few practical rules help avoid expensive detours:

- Don't optimize for one customer if you're expanding in the EU. A narrow custom format often creates future conversion work.

- Don't choose hybrid just because users like PDFs. Hybrid works when the receiving side accepts it and your team validates the embedded XML properly.

- Don't assume direct email is enough. If the recipient's process is network- or portal-based, email becomes a side channel, not the legal or operational one.

The best e invoicing format is usually the one that minimizes rework across your full invoice lifecycle, not just at document creation.

Implementation Best Practices for Finance and IT

The technical format is only one part of success. Most failures happen in the surrounding process. Poor master data, weak validation, and unclear exception ownership cause more trouble than the XML tag names.

What finance teams should fix first

Finance teams should begin with data quality and exception design.

If customer master data is inconsistent, automation will surface the problem quickly. Missing buyer references, incorrect tax identifiers, mismatched legal entity names, or inconsistent payment terms can all trigger rejection even when the format itself is valid.

A practical finance checklist looks like this:

- Clean recipient master data: Standard names and identifiers need to match what the buyer or portal expects.

- Define rejection ownership: Someone must own correction, resend, and communication when validation fails.

- Separate display from legal content: The PDF view is helpful, but the structured invoice fields are what downstream systems process.

- Review approval logic: Automated routing only works if invoice fields are consistently populated.

For teams evaluating broader process automation around invoice handling, this article on NZ businesses saving with AI automation is helpful as a process perspective, even though the regulatory environment differs from Austria.

What IT teams should validate before go-live

Hybrid e-invoice formats like Factur-X and ZUGFeRD embed structured XML inside a PDF/A-3 container. Novutech's technical guide to hybrid invoice formats notes why that matters operationally: the PDF remains human-readable, but compliance still depends on the embedded structured payload, and malformed XML can cause automated acceptance to fail even when the document looks correct.

That principle applies beyond hybrid documents. IT should validate more than syntax:

- Schema conformity: Does the invoice meet the required technical structure?

- Business rule compliance: Are mandatory fields, code lists, and country-specific rules satisfied?

- Transmission compatibility: Can the file move through the target network or portal without conversion errors?

- Archiving integrity: Is the legal invoice retained in a way that preserves the structured content?

A simple conceptual comparison helps. In a PDF, a line item appears as text in a table. In structured XML, the system receives clearly defined fields such as item identifier, quantity, unit price, tax category, and line total. The receiving application doesn't need to guess what each value means.

If you need a platform layer between ERP output and compliance requirements, providers in this space typically handle mapping, validation, transmission, and archiving. One example is integration approaches for existing finance systems, where middleware or e-invoicing services can bridge current ERP capabilities with Austrian and EU format requirements. Advintek Global is one such option for creating, validating, sending, and archiving invoices in line with Austrian compliance workflows.

The cleanest implementation is rarely the one with the fewest files. It's the one with the fewest manual exceptions.

Common Questions on E-Invoicing Formats

Is Peppol a format or a delivery network

It's best treated as a delivery network with its own implementation rules, not as a generic synonym for every e-invoice. In practice, businesses often send a structured invoice profile over that network. The network and the format are related, but they aren't the same thing.

Can you email an XML invoice

Sometimes yes, but that doesn't mean you should. Email may work in a private bilateral arrangement if the recipient accepts that method and can ingest the file reliably. It won't satisfy cases where the customer, network, or public process requires a specific transmission channel.

Do you need different formats for different countries

Often, yes. Even when countries share a common structured foundation, the accepted profile, mandatory fields, business rules, and delivery method can differ. The safest assumption is that cross-border invoicing needs a country-by-country acceptance check.

Is a hybrid PDF enough for compliance

Only if the recipient accepts that hybrid model and the embedded structured payload is valid. The visible PDF doesn't rescue a noncompliant XML layer.

What should a finance director ask first

Ask four things: what format the recipient accepts, what channel they require, what data fields are mandatory, and what record must be archived as the legal invoice. Those answers usually determine the rest of the project.

If your team is dealing with Austrian or EU e-invoicing requirements, Advintek Global is a practical starting point for evaluating how to create, validate, deliver, and archive invoices without rebuilding your finance process from scratch.

Created with Outrank